Net Profit Forecasting

Overview:

This notebook aimed is to demonstrate the solution for simple regression problem, predict net profit given a set of attributes, first I start with simple EDA understand the data numerical and categorical distributions. Then I fit simple statistical model followed by linear regression and more complex one. each model includes scoring metrics and explanations. Finally, I communicate final finding of prediction of the provided Out-of-sample test set and the including factors or attributes that decided the final predictions using shapley values.

- Basic EDA.

- Feature Engineering.

- Statistical Model.

- Baseline Model

- Complex Model.

- Scoring.

- SHAPly Values, Interoperable ML.

# modeling

from sklearn.linear_model import LinearRegression

from lightgbm import LGBMRegressor

from statsmodels.regression.linear_model import OLS

from sklearn.model_selection import train_test_split

from sklearn.model_selection import StratifiedKFold

from sklearn.preprocessing import OneHotEncoder, LabelEncoder

# model diagnosis:

from yellowbrick.model_selection import learning_curve

from yellowbrick.regressor import ResidualsPlot

# Interpretable Machine Learning:

import shap

# helper functions I wrote for this dataset:

from utils import *

import warnings

warnings.filterwarnings('ignore')

# Settings and aesthetics:

cmap_data = plt.cm.Paired

cmap_cv = plt.cm.coolwarm

cmap_data = plt.cm.Paired

cmap_cv = plt.cm.coolwarm

# Some basic settings here:

pd.set_option('display.max_rows', 500)

pd.set_option('display.max_columns', 500)

pd.set_option('display.width', 1000)

pd.options.display.max_columns = 30

EDA

modeling_data = pd.read_csv("../../Data/labeled_dataset.csv")

modeling_data.set_index("index", inplace=True)

modeling_data.head()

| Age | Monthly premium | Socioeconomic category | Monthly kilometers | Coefficient bonus malus | Vehicle type | CRM score | Standard of living | Brand | Yearly income | Credit score | Yearly maintenance cost | Net profit | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| index | |||||||||||||

| 0 | 58.0 | 40.0 | Student | 973 | 106 | SUV | 164 | 3762 | Peugeot | 20420 | 309 | 801 | 54.998558 |

| 1 | 26.0 | 27.0 | Labor worker | 637 | 95 | 5 doors | 126 | 3445 | Renault | 25750 | 135 | 667 | 7.840930 |

| 2 | 27.0 | 26.0 | Office worker | 978 | 136 | SUV | 153 | 986 | Renault | 6790 | 786 | 696 | 46.078889 |

| 3 | 22.0 | 8.0 | Student | 771 | 96 | 3 doors | 111 | 2366 | Peugeot | 15140 | 320 | 765 | -11.048213 |

| 4 | 60.0 | 20.0 | Unemployed | 758 | 101 | 3 doors | 149 | 1441 | Peugeot | 12850 | 287 | 808 | 1.180078 |

modeling_data.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 1000 entries, 0 to 999

Data columns (total 13 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Age 983 non-null float64

1 Monthly premium 989 non-null float64

2 Socioeconomic category 1000 non-null object

3 Monthly kilometers 1000 non-null int64

4 Coefficient bonus malus 1000 non-null int64

5 Vehicle type 1000 non-null object

6 CRM score 1000 non-null int64

7 Standard of living 1000 non-null int64

8 Brand 948 non-null object

9 Yearly income 1000 non-null int64

10 Credit score 1000 non-null int64

11 Yearly maintenance cost 1000 non-null int64

12 Net profit 1000 non-null float64

dtypes: float64(3), int64(7), object(3)

memory usage: 109.4+ KB

modeling_data.isnull().sum().to_frame().style.background_gradient(cmap='summer')

| 0 | |

|---|---|

| Age | 17 |

| Monthly premium | 11 |

| Socioeconomic category | 0 |

| Monthly kilometers | 0 |

| Coefficient bonus malus | 0 |

| Vehicle type | 0 |

| CRM score | 0 |

| Standard of living | 0 |

| Brand | 52 |

| Yearly income | 0 |

| Credit score | 0 |

| Yearly maintenance cost | 0 |

| Net profit | 0 |

# fill nan with other Brand types:

modeling_data["Brand"].fillna("other", inplace=True)

modeling_data = modeling_data[modeling_data["Monthly premium"].notna()]

modeling_data.columns.tolist()

['Age',

'Monthly premium',

'Socioeconomic category',

'Monthly kilometers',

'Coefficient bonus malus',

'Vehicle type',

'CRM score',

'Standard of living',

'Brand',

'Yearly income',

'Credit score',

'Yearly maintenance cost',

'Net profit']

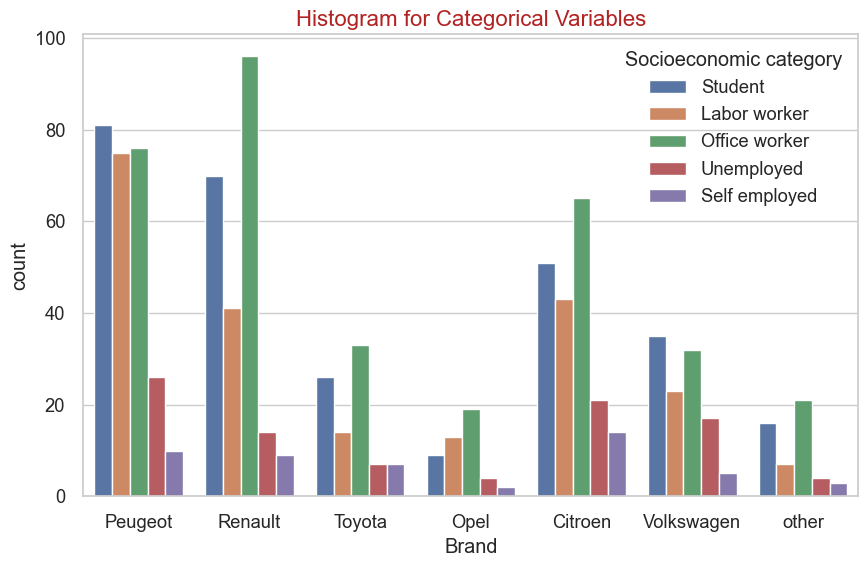

plt.figure(figsize=(10,6))

sns.set(style="whitegrid", font_scale=1.2)

chart = sns.countplot(x='Brand',

hue='Socioeconomic category',

data=modeling_data,

palette='deep')

chart.set_title('Histogram for Categorical Variables', fontsize=16, color='firebrick')

plt.show()

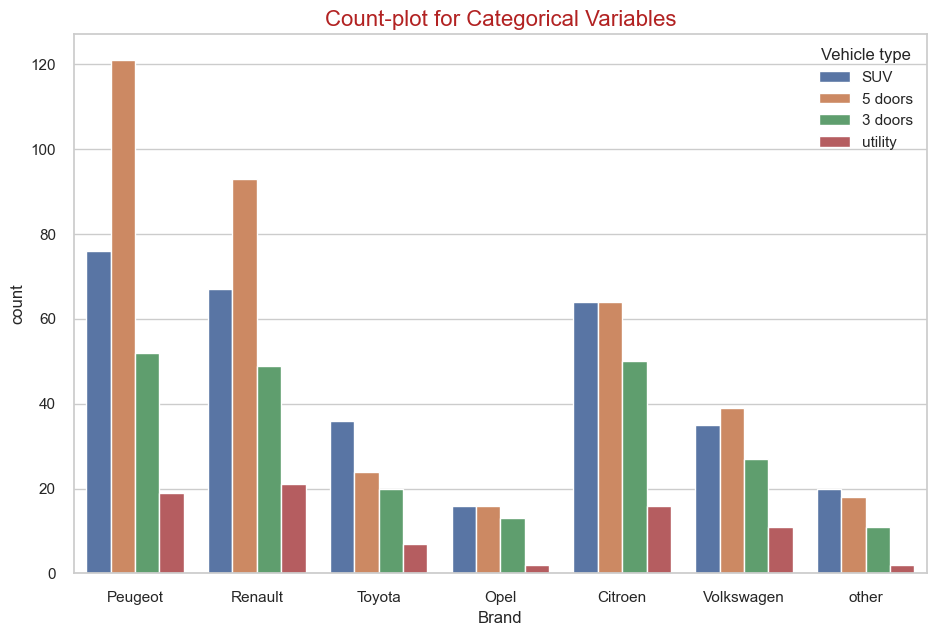

sns.set(style="whitegrid")

plt.figure(figsize=(11,7))

chart = sns.countplot(x='Brand',

hue='Vehicle type',

data=modeling_data,

palette='deep')

chart.set_title('Count-plot for Categorical Variables', fontsize=16, color='firebrick')

plt.show()

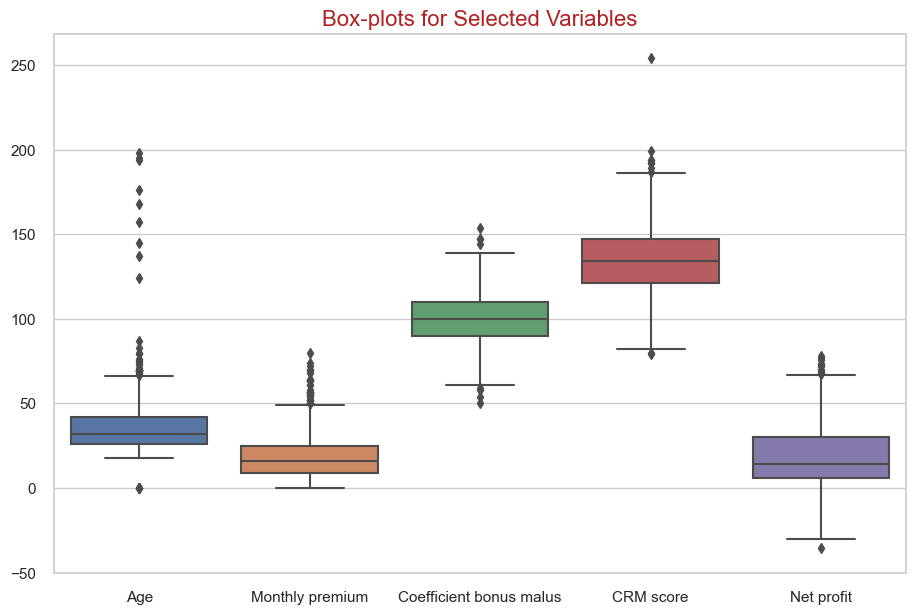

plt.figure(figsize=(11,7))

sns.boxplot(data=modeling_data[["Age",

"Monthly premium",

"Coefficient bonus malus",

"CRM score",

"Net profit"]])

plt.title('Box-plots for Selected Variables', fontsize=16, color='firebrick')

plt.show()

# drop extreme outlier from the above observations:

modeling_data = modeling_data[modeling_data["CRM score"] < 254]

modeling_data = modeling_data[(modeling_data["Age"] < 124) & (modeling_data["Age"] > 0)]

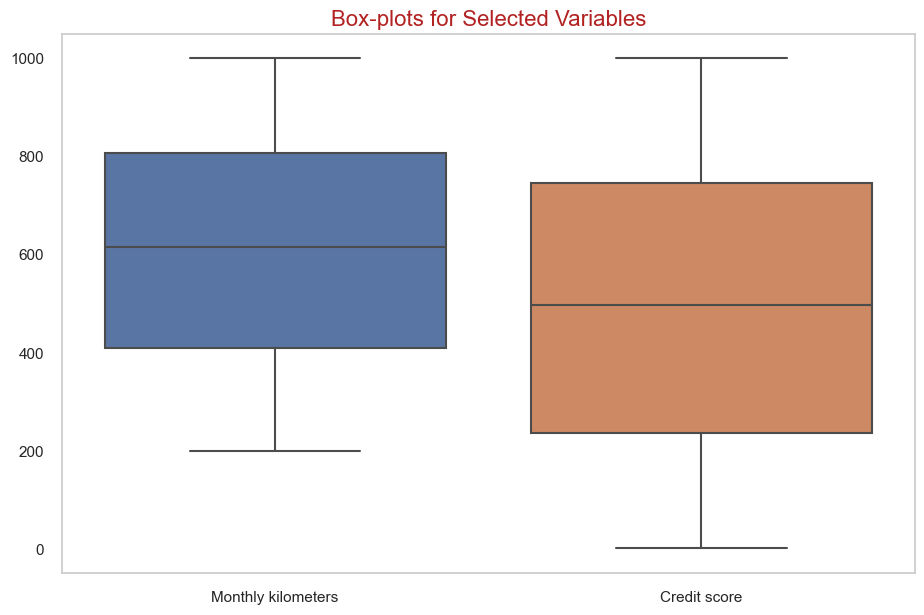

# no warning outlier for credit score, monthly kilometers and yearly maintenance cost:

plt.figure(figsize=(11,7))

sns.boxplot(data=modeling_data[["Monthly kilometers", "Credit score"]])

plt.title('Box-plots for Selected Variables', fontsize=16, color='firebrick')

plt.grid(False)

plt.show()

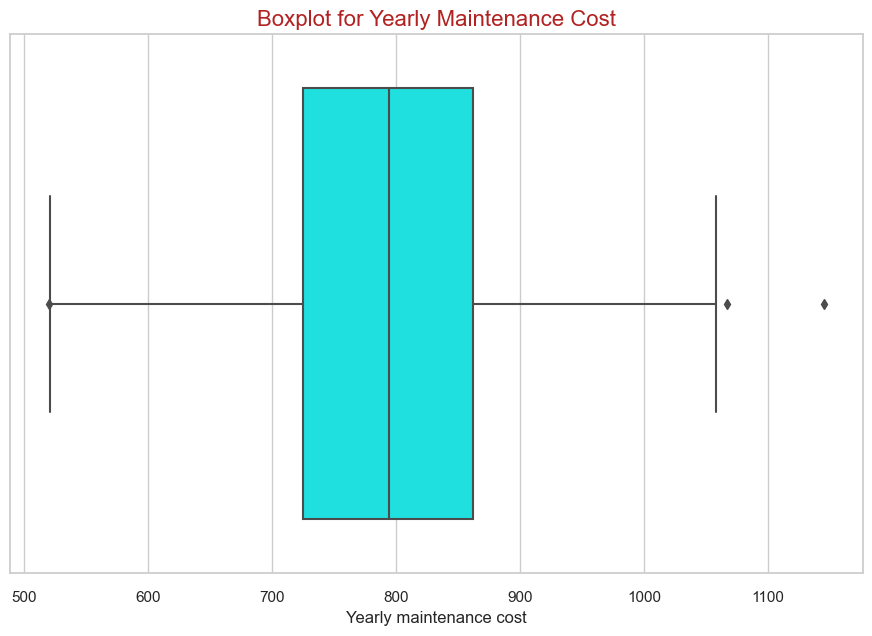

plt.figure(figsize=(11,7))

sns.boxplot(x=modeling_data["Yearly maintenance cost"], color='aqua')

plt.title('Boxplot for Yearly Maintenance Cost', fontsize=16, color='firebrick')

plt.show()

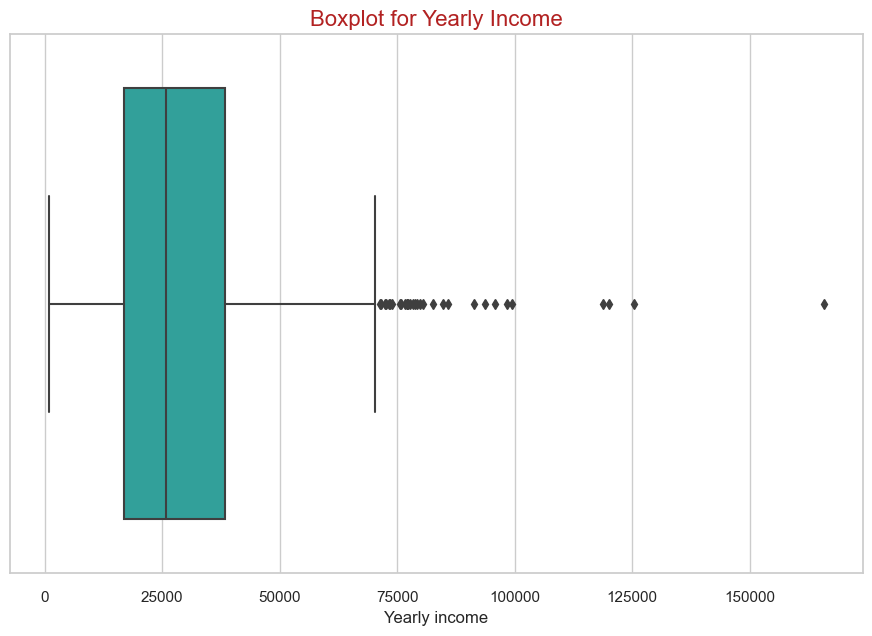

plt.figure(figsize=(11,7))

sns.boxplot(x=modeling_data["Yearly income"], color='lightseagreen')

plt.title('Boxplot for Yearly Income', fontsize=16, color='firebrick')

plt.show()

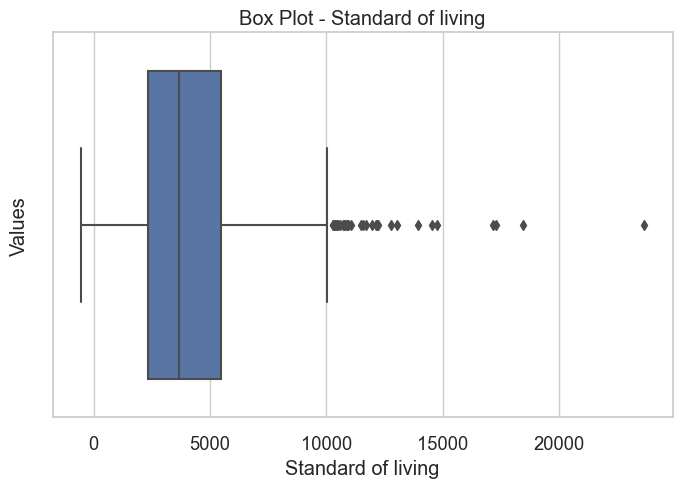

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 5))

sns.boxplot(x=modeling_data["Standard of living"])

plt.xlabel("Standard of living")

plt.ylabel("Values")

plt.title("Box Plot - Standard of living")

plt.show()

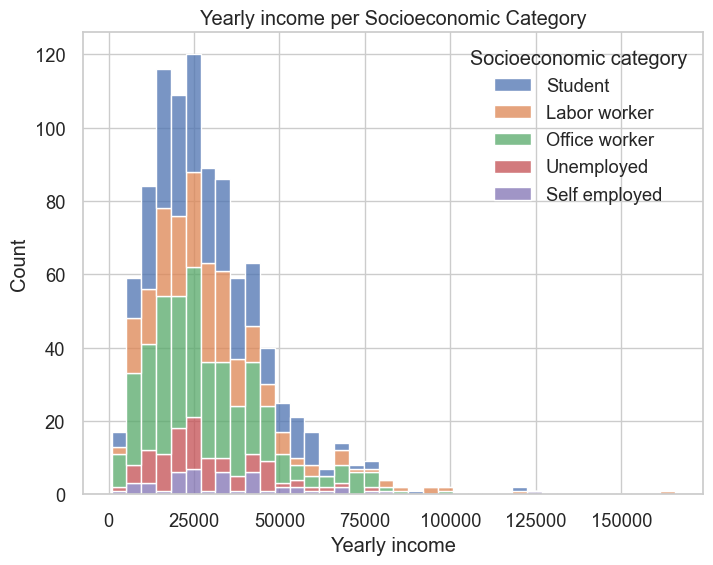

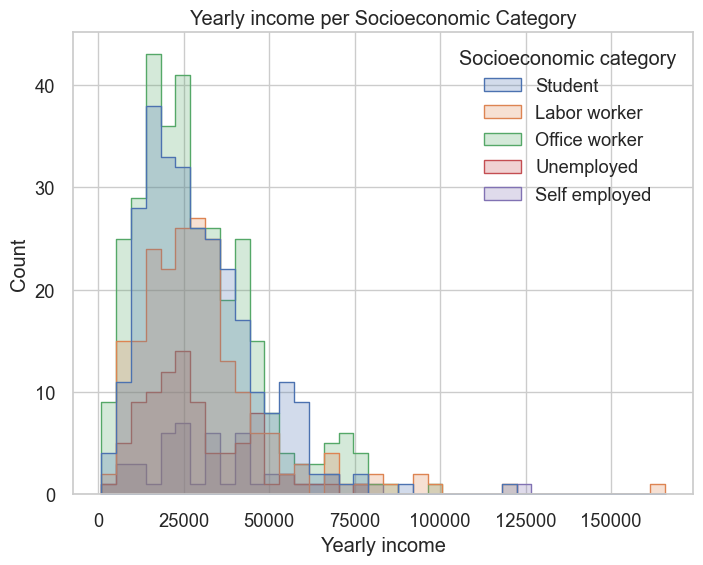

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 6))

sns.histplot(data=modeling_data, x="Yearly income", hue="Socioeconomic category", multiple="stack")

plt.xlabel("Yearly income")

plt.ylabel("Count")

plt.title("Yearly income per Socioeconomic Category")

plt.show()

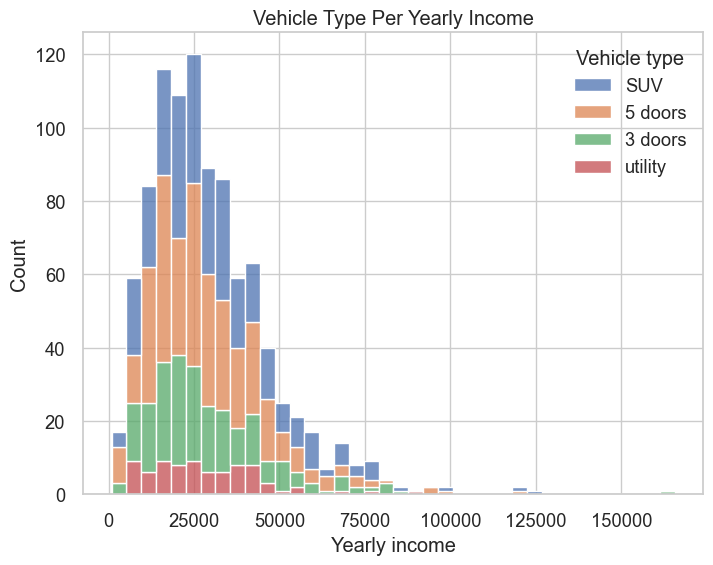

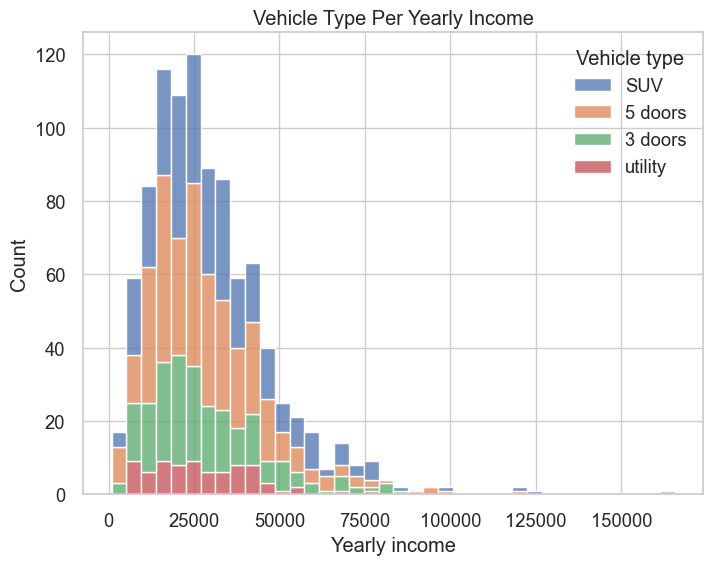

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 6))

sns.histplot(data=modeling_data, x="Yearly income", hue="Vehicle type", multiple="stack")

plt.xlabel("Yearly income")

plt.ylabel("Count")

plt.title("Vehicle Type Per Yearly Income")

plt.show()

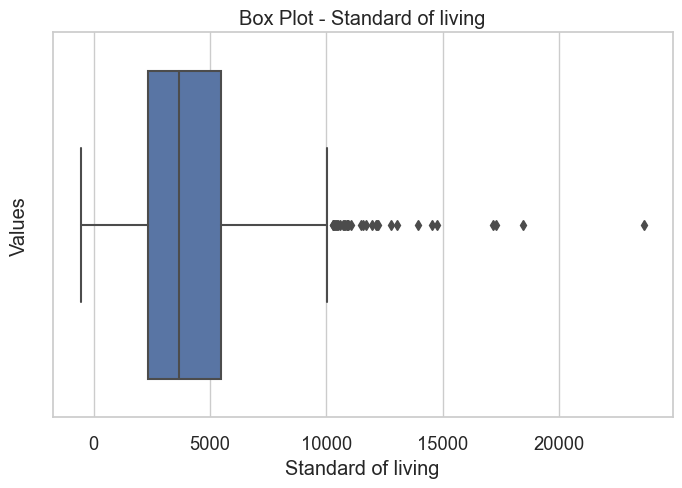

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 5))

sns.boxplot(x=modeling_data["Standard of living"])

plt.xlabel("Standard of living")

plt.ylabel("Values")

plt.title("Box Plot - Standard of living")

plt.show()

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 6))

sns.histplot(data=modeling_data, x="Yearly income", hue="Socioeconomic category", element="step")

plt.xlabel("Yearly income")

plt.ylabel("Count")

plt.title("Yearly income per Socioeconomic Category")

plt.show()

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 6))

sns.histplot(data=modeling_data, x="Yearly income", hue="Vehicle type", multiple="stack")

plt.xlabel("Yearly income")

plt.ylabel("Count")

plt.title("Vehicle Type Per Yearly Income")

plt.show()

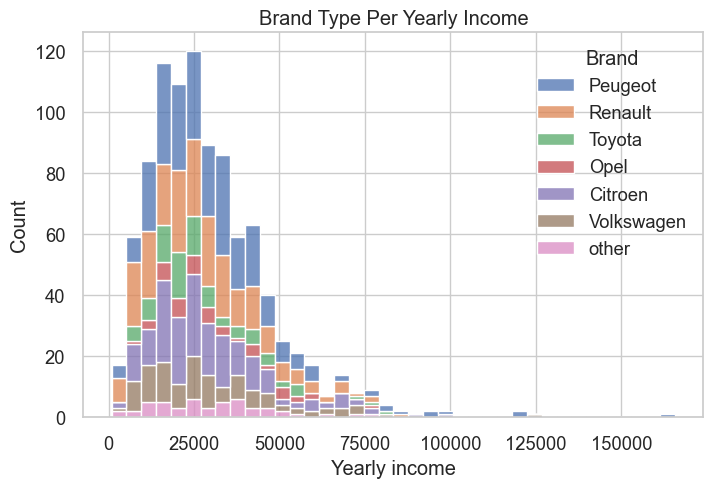

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 5))

sns.histplot(data=modeling_data, x="Yearly income", hue="Brand", multiple="stack")

plt.xlabel("Yearly income")

plt.ylabel("Count")

plt.title("Brand Type Per Yearly Income")

plt.show()

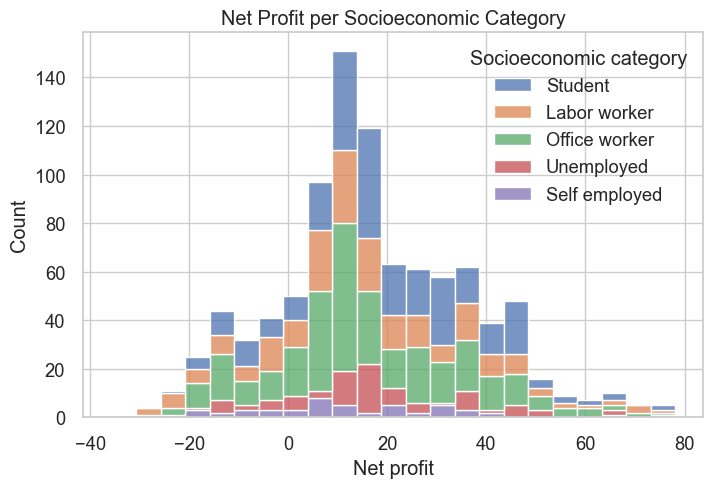

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 5))

sns.histplot(data=modeling_data, x="Net profit", hue="Socioeconomic category", multiple="stack")

plt.xlabel("Net profit")

plt.ylabel("Count")

plt.title("Net Profit per Socioeconomic Category")

plt.show()

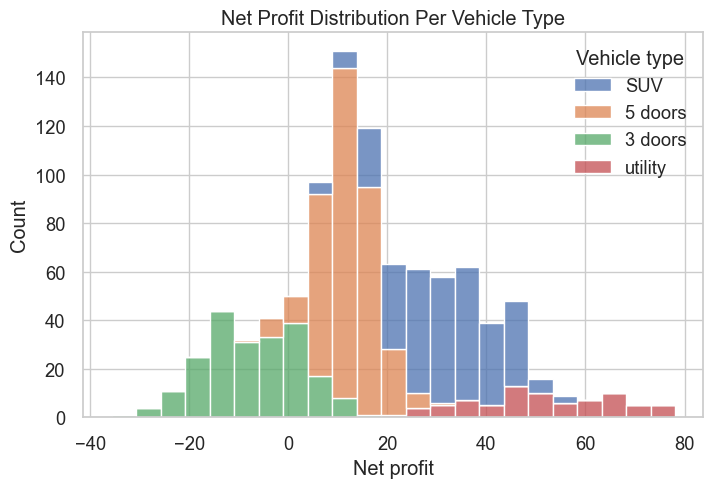

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 5))

sns.histplot(data=modeling_data, x="Net profit", hue="Vehicle type", multiple="stack")

plt.xlabel("Net profit")

plt.ylabel("Count")

plt.title("Net Profit Distribution Per Vehicle Type")

plt.show()

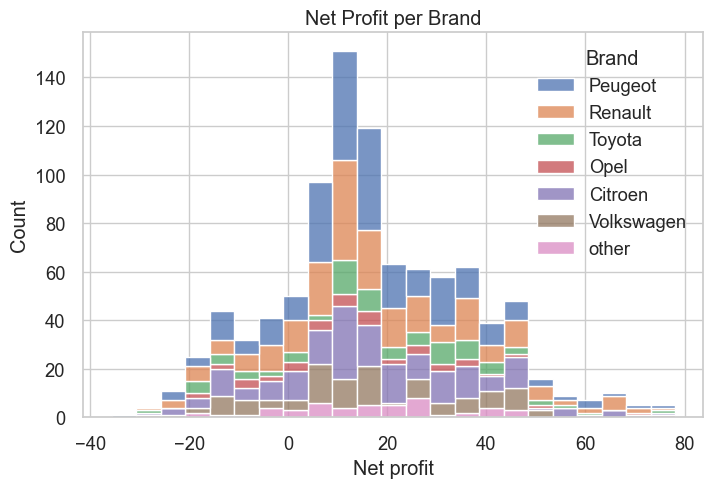

sns.set(style="whitegrid", font_scale=1.2)

plt.figure(figsize=(8, 5))

sns.histplot(data=modeling_data, x="Net profit", hue="Brand", multiple="stack")

plt.xlabel("Net profit")

plt.ylabel("Count")

plt.title("Net Profit per Brand")

plt.show()

Observations:

- No warning outliers seen in the data except for yearly income, CRM score and Age.

- Numerical data are normally distributed.

Encode categorical variables and clean data for modeling:

# categorize your variables here:

categories = [

'Brand',

'Vehicle type',

'Socioeconomic category',

]

modeling_data_visualization = pd.get_dummies(modeling_data,

columns=categories,

drop_first=True)

modeling_data = pd.get_dummies(

modeling_data,

columns=categories,

drop_first=True

)

# rearrange columns:

ordered_corr_columns = modeling_data_visualization.copy()

ordered_corr_columns = ordered_corr_columns[['Age',

'Monthly premium',

'Monthly kilometers',

'Coefficient bonus malus',

'CRM score',

'Standard of living',

'Yearly income',

'Credit score',

'Yearly maintenance cost',

'Brand_Citroen',

'Brand_Opel',

'Brand_Peugeot',

'Brand_Renault',

'Brand_Toyota',

'Brand_Volkswagen',

'Brand_other',

'Vehicle type_3 doors',

'Vehicle type_5 doors',

'Vehicle type_SUV',

'Vehicle type_utility',

'Socioeconomic category_Labor worker',

'Socioeconomic category_Office worker',

'Socioeconomic category_Self employed',

'Socioeconomic category_Student',

'Socioeconomic category_Unemployed',

'Net profit'

]]

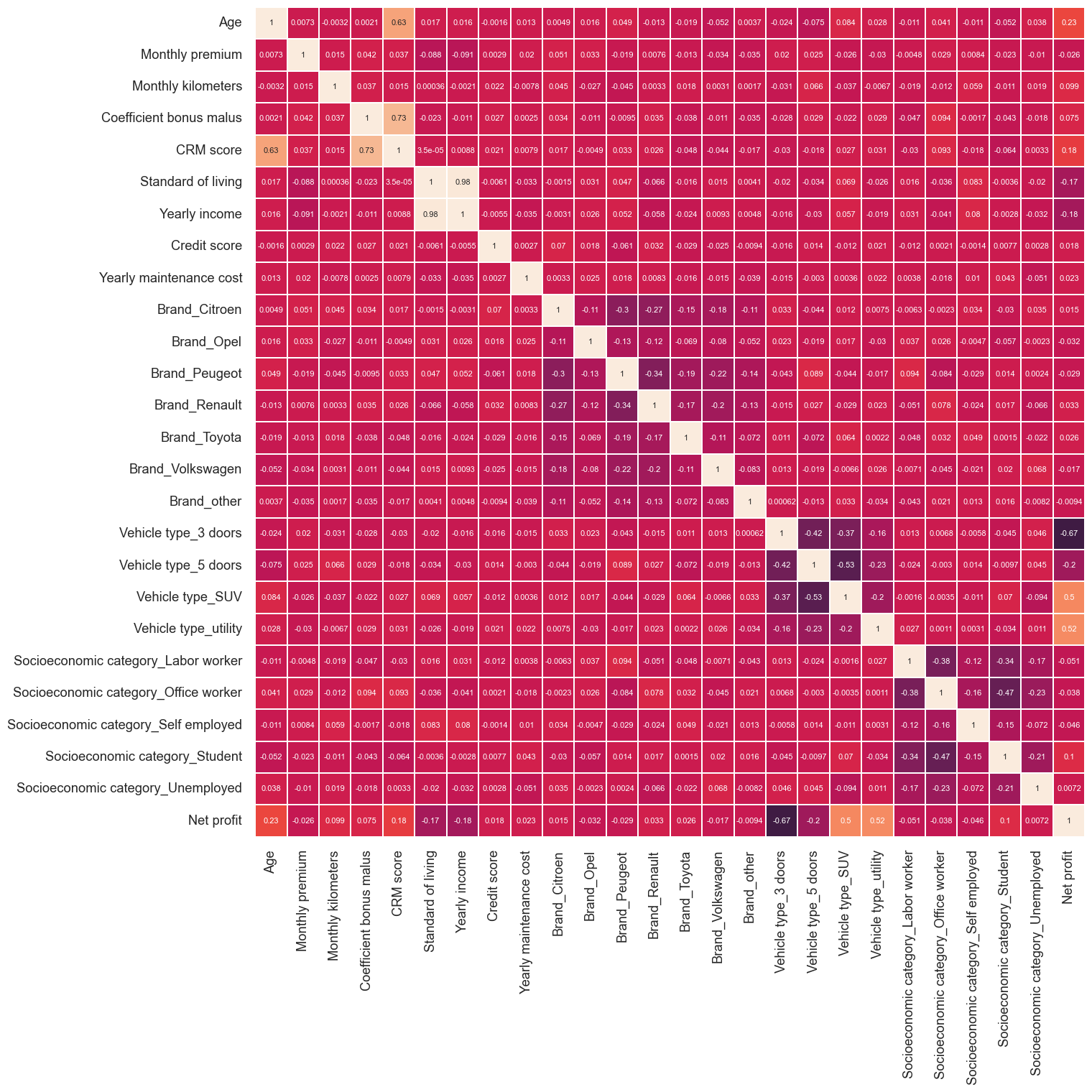

plt.figure(figsize=(15, 15))

corr = ordered_corr_columns.corr()

corr_top = corr.index

sns.heatmap(modeling_data_visualization[corr_top].corr(),

vmax=1.0,

vmin=-1.0,

linewidths=0.1,

annot=True,

annot_kws={"size": 8},

square=True, cbar=False);

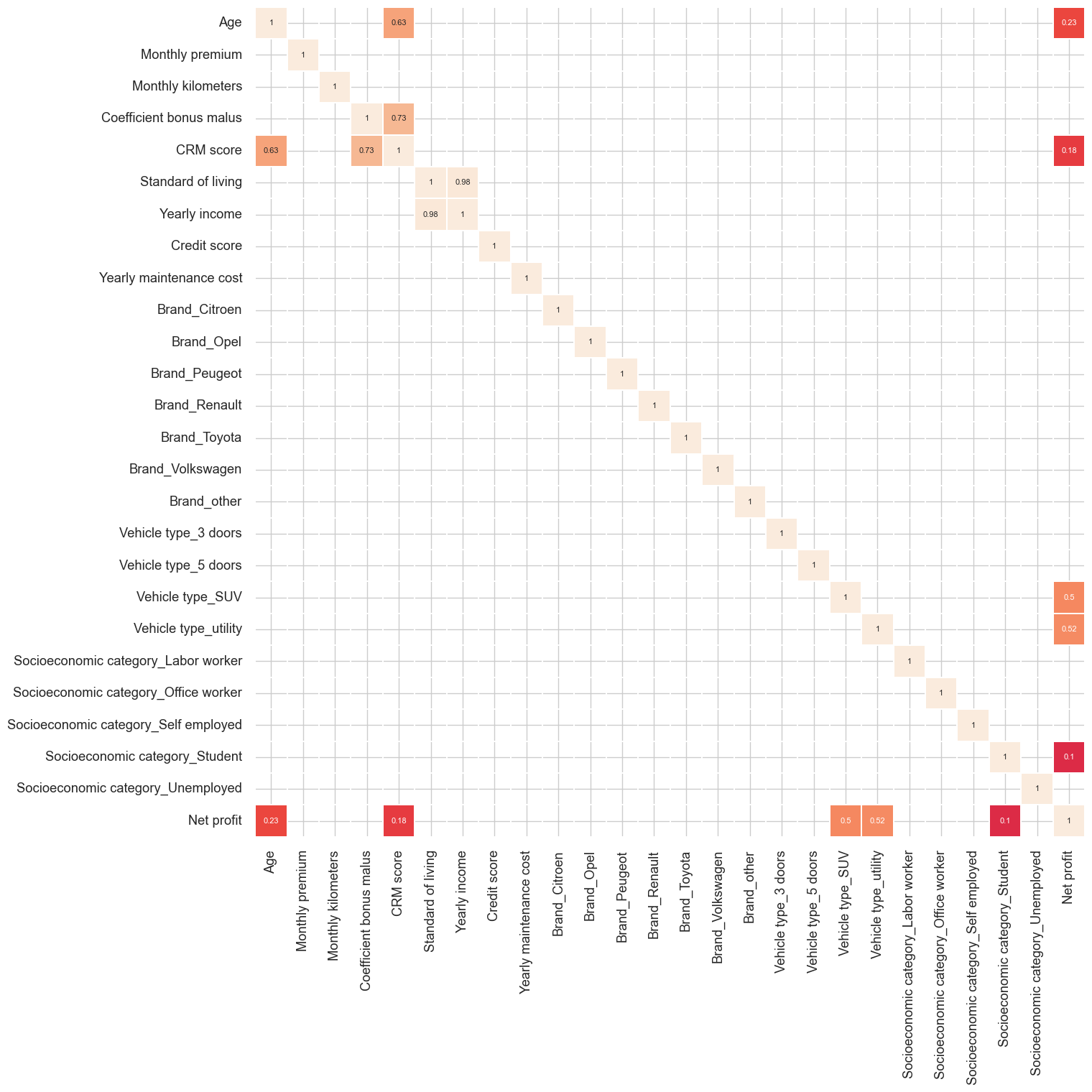

corr = ordered_corr_columns.corr()

plt.figure(figsize=(15, 15))

sns.heatmap(corr[(corr >= 0.1)],

vmax=1.0,

vmin=-1.0,

linewidths=0.1,

annot=True,

annot_kws={"size": 8},

square=True,

cbar=False)

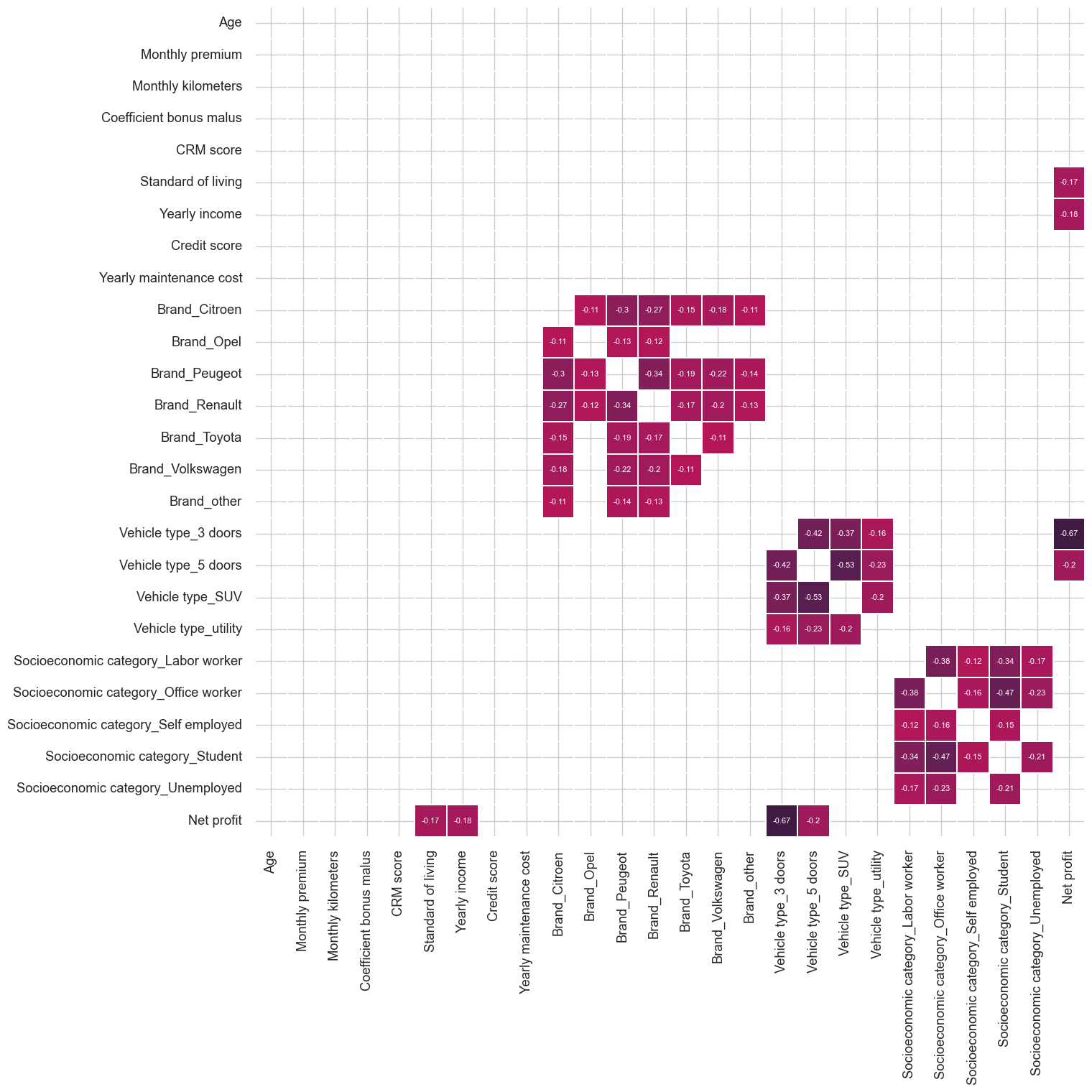

corr = ordered_corr_columns.corr()

plt.figure(figsize=(15, 15))

sns.heatmap(corr[(corr <= -0.1)],

vmax=1.0,

vmin=-1.0,

linewidths=0.1,

annot=True,

annot_kws={"size": 8},

square=True,

cbar=False);

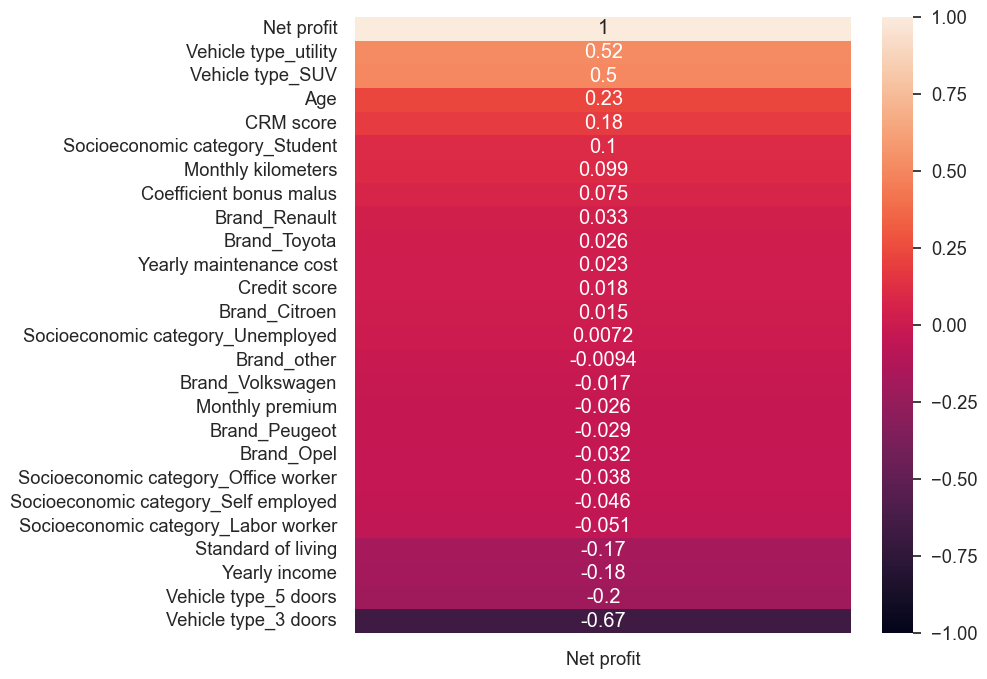

fig, ax = plt.subplots(figsize=(8, 8))

sns.heatmap(modeling_data_visualization.corr()[["Net profit"]].sort_values("Net profit"),

vmax=1,

vmin=-1,

annot=True,

ax=ax)

ax.invert_yaxis()

Observations:

- There is not any warning high correlation between target variable and independent variables.

- Multi-collinearity between Standard of living and yearly income, CRM score and Coefficient bonus malus, they might be problematic for linear models interpretation.

- There are few independent variables can be used for fitting model that correlate positively/negatively with Net profit.

- There is enough signals in the data simple model with fewer coefficient would generalize on unseen data.

Simple Model:

Features = modeling_data.columns.tolist()

Features.remove("Net profit")

Ys = modeling_data["Net profit"]

Xs = modeling_data[Features]

Multi-collinearity Check VIF:

calculate_vif(Xs).style.background_gradient(cmap='summer')

| variables | VIF | |

|---|---|---|

| 0 | Age | 63.237779 |

| 1 | Monthly premium | 3.050082 |

| 2 | Monthly kilometers | 7.627456 |

| 3 | Coefficient bonus malus | 432.507997 |

| 4 | CRM score | 718.673947 |

| 5 | Standard of living | 110.184626 |

| 6 | Yearly income | 115.704855 |

| 7 | Credit score | 3.866306 |

| 8 | Yearly maintenance cost | 35.804418 |

| 9 | Brand_Opel | 1.240398 |

| 10 | Brand_Peugeot | 2.379924 |

| 11 | Brand_Renault | 2.191521 |

| 12 | Brand_Toyota | 1.432597 |

| 13 | Brand_Volkswagen | 1.562894 |

| 14 | Brand_other | 1.252540 |

| 15 | Vehicle type_5 doors | 2.692416 |

| 16 | Vehicle type_SUV | 2.464803 |

| 17 | Vehicle type_utility | 1.374975 |

| 18 | Socioeconomic category_Office worker | 2.635837 |

| 19 | Socioeconomic category_Self employed | 1.248430 |

| 20 | Socioeconomic category_Student | 2.359763 |

| 21 | Socioeconomic category_Unemployed | 1.440898 |

fixed_Xs = Xs.drop(["Standard of living",

"Coefficient bonus malus",

"CRM score",

"Yearly maintenance cost"], axis=1)

calculate_vif(fixed_Xs).style.background_gradient(cmap='summer')

| variables | VIF | |

|---|---|---|

| 0 | Age | 7.099762 |

| 1 | Monthly premium | 2.836646 |

| 2 | Monthly kilometers | 6.413401 |

| 3 | Yearly income | 3.427115 |

| 4 | Credit score | 3.583600 |

| 5 | Brand_Opel | 1.204267 |

| 6 | Brand_Peugeot | 2.175342 |

| 7 | Brand_Renault | 2.026626 |

| 8 | Brand_Toyota | 1.377058 |

| 9 | Brand_Volkswagen | 1.472219 |

| 10 | Brand_other | 1.225380 |

| 11 | Vehicle type_5 doors | 2.558872 |

| 12 | Vehicle type_SUV | 2.345649 |

| 13 | Vehicle type_utility | 1.333014 |

| 14 | Socioeconomic category_Office worker | 2.430892 |

| 15 | Socioeconomic category_Self employed | 1.226225 |

| 16 | Socioeconomic category_Student | 2.203248 |

| 17 | Socioeconomic category_Unemployed | 1.386635 |

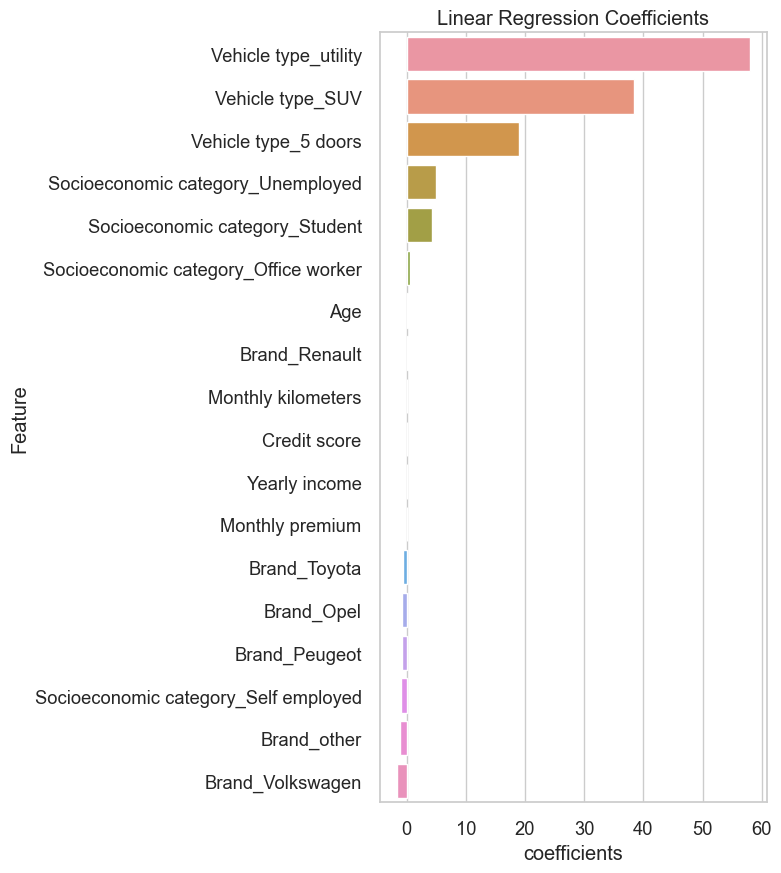

simple_model = LinearRegression().fit(fixed_Xs, Ys)

simple_model.score(fixed_Xs, Ys)

0.8834266631920002

coef = get_regressor_coefficients(simple_model, fixed_Xs.columns.tolist())

coefficient_plot(coef.values(), coef.keys())

est = OLS(Ys, Xs).fit()

print(est.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: Net profit R-squared (uncentered): 0.930

Model: OLS Adj. R-squared (uncentered): 0.929

Method: Least Squares F-statistic: 569.0

Date: Mon, 26 Jun 2023 Prob (F-statistic): 0.00

Time: 15:46:44 Log-Likelihood: -3203.3

No. Observations: 958 AIC: 6451.

Df Residuals: 936 BIC: 6558.

Df Model: 22

Covariance Type: nonrobust

========================================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------------------

Age 0.2148 0.048 4.474 0.000 0.121 0.309

Monthly premium -0.0320 0.017 -1.875 0.061 -0.066 0.002

Monthly kilometers 0.0072 0.001 7.597 0.000 0.005 0.009

Coefficient bonus malus -0.0124 0.046 -0.270 0.787 -0.103 0.078

CRM score 0.0156 0.044 0.354 0.724 -0.071 0.102

Standard of living 0.0003 0.000 0.566 0.572 -0.001 0.001

Yearly income -0.0003 6.95e-05 -3.946 0.000 -0.000 -0.000

Credit score -0.0010 0.001 -1.340 0.181 -0.003 0.000

Yearly maintenance cost -0.0139 0.002 -8.276 0.000 -0.017 -0.011

Brand_Opel -1.5706 1.151 -1.364 0.173 -3.830 0.689

Brand_Peugeot -1.7943 0.666 -2.694 0.007 -3.101 -0.487

Brand_Renault -0.7600 0.683 -1.113 0.266 -2.100 0.580

Brand_Toyota -1.7598 0.905 -1.943 0.052 -3.537 0.017

Brand_Volkswagen -2.6734 0.830 -3.220 0.001 -4.303 -1.044

Brand_other -2.2858 1.109 -2.062 0.039 -4.461 -0.110

Vehicle type_5 doors 18.3364 0.600 30.537 0.000 17.158 19.515

Vehicle type_SUV 37.8587 0.621 60.937 0.000 36.639 39.078

Vehicle type_utility 57.4583 0.921 62.415 0.000 55.652 59.265

Socioeconomic category_Office worker -0.2975 0.620 -0.480 0.631 -1.514 0.919

Socioeconomic category_Self employed -1.5587 1.130 -1.379 0.168 -3.776 0.659

Socioeconomic category_Student 3.5937 0.633 5.676 0.000 2.351 4.836

Socioeconomic category_Unemployed 3.9310 0.887 4.431 0.000 2.190 5.672

==============================================================================

Omnibus: 15.750 Durbin-Watson: 1.959

Prob(Omnibus): 0.000 Jarque-Bera (JB): 24.111

Skew: -0.131 Prob(JB): 5.81e-06

Kurtosis: 3.731 Cond. No. 2.28e+05

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[3] The condition number is large, 2.28e+05. This might indicate that there are

strong multicollinearity or other numerical problems.

statistical_results_as_frame = get_dataframe_from_summary(est)

statistical_results_as_frame[statistical_results_as_frame["P>|t|"] <= 0.000].

style.background_gradient(cmap='summer')

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Age | 0.214800 | 0.048000 | 4.474000 | 0.000000 | 0.121000 | 0.309000 |

| Monthly kilometers | 0.007200 | 0.001000 | 7.597000 | 0.000000 | 0.005000 | 0.009000 |

| Yearly income | -0.000300 | 0.000069 | -3.946000 | 0.000000 | -0.000000 | -0.000000 |

| Yearly maintenance cost | -0.013900 | 0.002000 | -8.276000 | 0.000000 | -0.017000 | -0.011000 |

| Vehicle type_5 doors | 18.336400 | 0.600000 | 30.537000 | 0.000000 | 17.158000 | 19.515000 |

| Vehicle type_SUV | 37.858700 | 0.621000 | 60.937000 | 0.000000 | 36.639000 | 39.078000 |

| Vehicle type_utility | 57.458300 | 0.921000 | 62.415000 | 0.000000 | 55.652000 | 59.265000 |

| Socioeconomic category_Student | 3.593700 | 0.633000 | 5.676000 | 0.000000 | 2.351000 | 4.836000 |

| Socioeconomic category_Unemployed | 3.931000 | 0.887000 | 4.431000 | 0.000000 | 2.190000 | 5.672000 |

X_train, X_test, y_train, y_test = train_test_split(fixed_Xs,

Ys,

test_size=0.3,

random_state=10101)

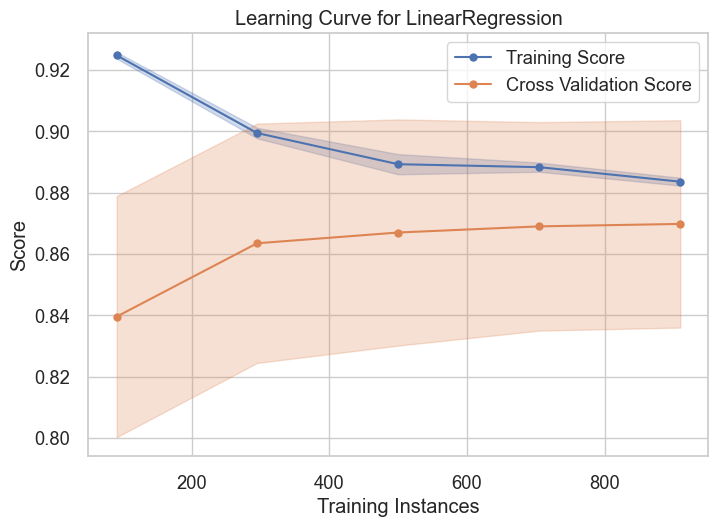

visualizer = LearningCurve(

simple_model, cv=20, scoring='r2',

n_jobs=4

)

visualizer.fit(fixed_Xs,Ys )

visualizer.show()

<Axes: title={'center': 'Learning Curve for LinearRegression'}, xlabel='Training Instances', ylabel='Score'>

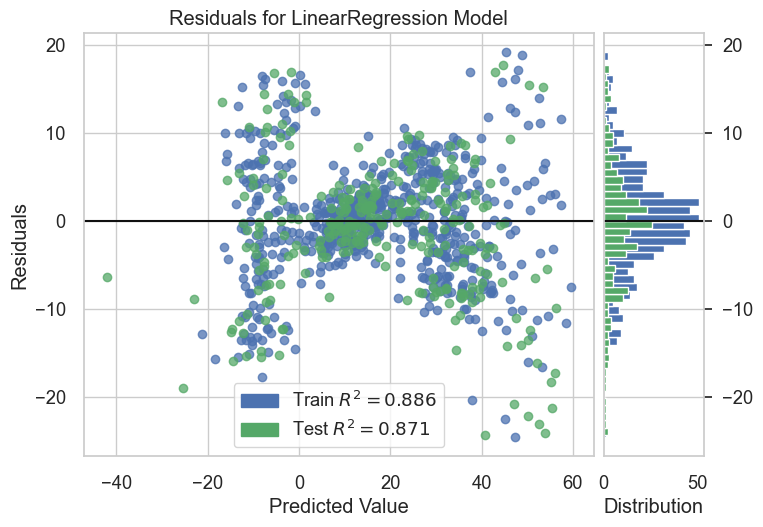

model = LinearRegression()

visualizer = ResidualsPlot(model)

visualizer.fit(X_train, y_train)

visualizer.score(X_test, y_test)

visualizer.show()

<Axes: title={'center': 'Residuals for LinearRegression Model'}, xlabel='Predicted Value', ylabel='Residuals'>

Observations:

- As suspected Standard of living, yearly income and Coefficient bonus malus has strong correlation with other independent variables, they can be predicted by other independent variables.

- As suspected model is stable against few features, after dropping independent variables with high VIF scores 0.886

- P-values: Socioeconomic: student, unemployed, vehicle types 3,5 suv and utility, yearly income, age and monthly kilometers suggest strong significant relation between them and target variable on large populations.

- Brand Renault and Toyota P-values suggest strong influence on target variable compared to other brands.

- Residuals: indicates a good fit for linear model, predicted values greater than 40 are misfit for compared to the training samples.

- unexpected high p-value for Socioeconomic Self employed brand Volkswagen, Credit score and Yearly maintenance cost independent variables.

- Model tend to generalize when applying cross-validation of 20 folds, testing and training scores are matching after 20 folds/iterations.

Complex Model:

- From the above observation we have constructed a stable model with simple features and linear repressor, I would vote for simplified models since they are easy to explain to stakeholders and easier to productionize compared to more complex model with high variance.

- The fact that the data is synthetic and generated from known function makes it even easier to fit a model against normally distributed target variables.

- Tho it’s not required for this particular dataset but the demonstration below will help explain what is happening behind the scene why applying a particular predictions.

complex_model = LGBMRegressor(random_state=np.random.RandomState().get_state()[1][0])

complex_model.fit(X_train, y_train)

LGBMRegressor(random_state=2147483648)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

LGBMRegressor(random_state=2147483648)

{"training score": complex_model.score(X_train, y_train),

"testing score": complex_model.score(X_test, y_test)}

{'training score': 0.9954600929824392, 'testing score': 0.9744489721140687}

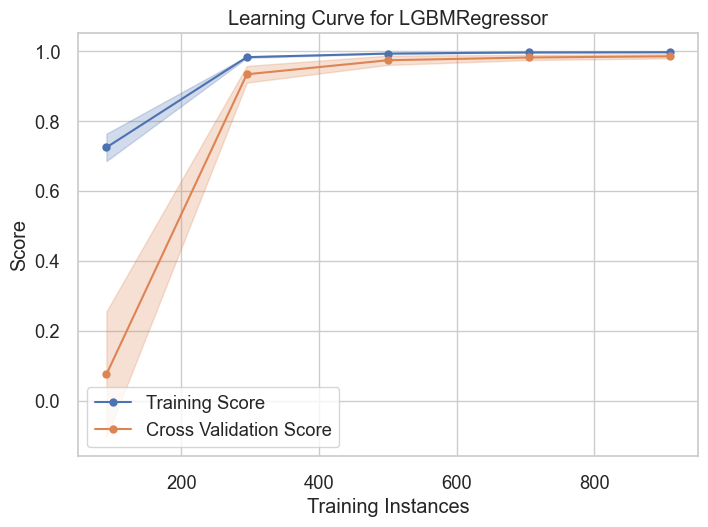

visualizer = LearningCurve(

complex_model,

cv=20,

scoring='r2',

n_jobs=4

)

visualizer.fit(fixed_Xs,Ys )

visualizer.show()

<Axes: title={'center': 'Learning Curve for LGBMRegressor'}, xlabel='Training Instances', ylabel='Score'>

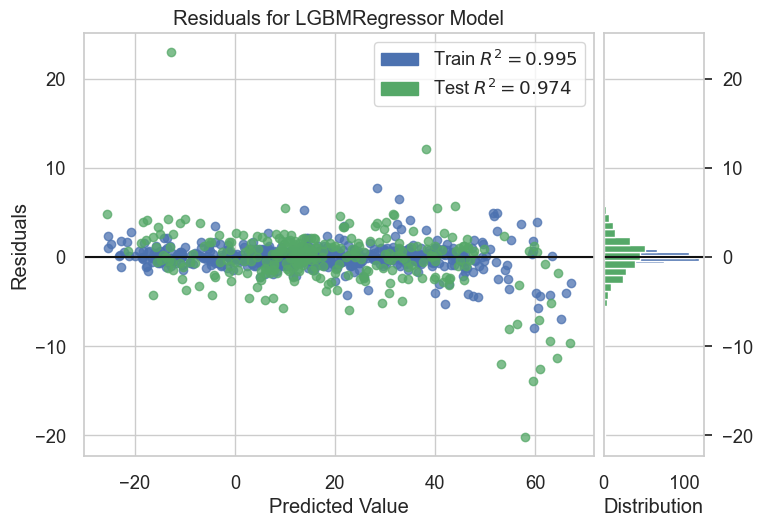

visualizer = ResidualsPlot(complex_model)

visualizer.fit(X_train, y_train)

visualizer.score(X_test, y_test)

visualizer.show()

<Axes: title={'center': 'Residuals for LGBMRegressor Model'}, xlabel='Predicted Value', ylabel='Residuals'>

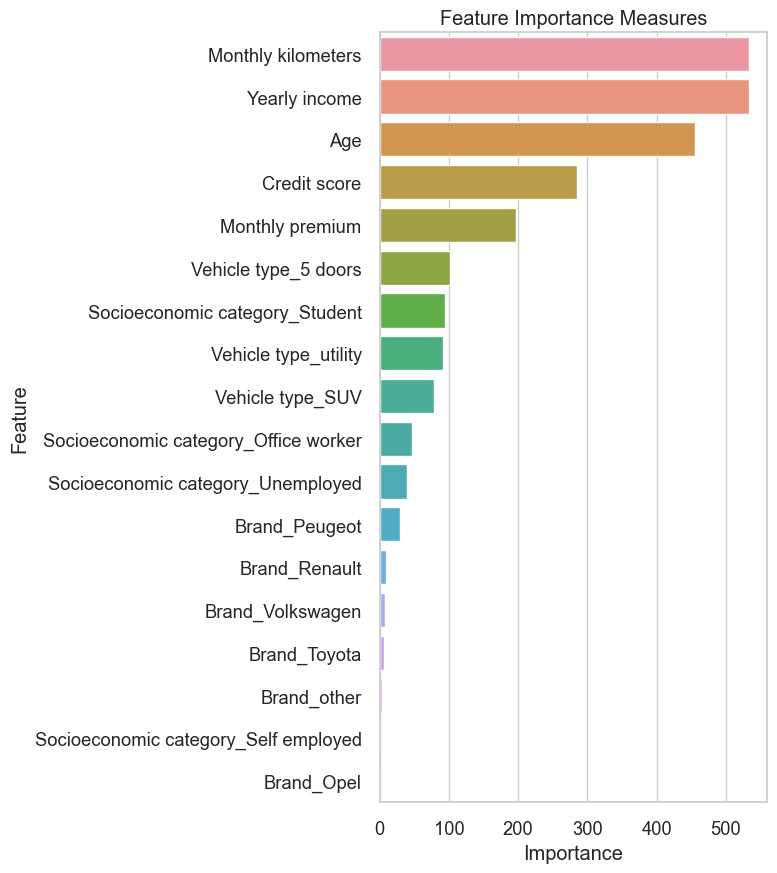

feature_importance_plot(complex_model.feature_importances_, X_train.columns.tolist())

X_train, X_test, y_train, y_test = train_test_split(fixed_Xs,

Ys,

test_size=0.3,

random_state=10101)

complex_model.fit(X_train, y_train)

complex_model.score(X_test, y_test)

0.9744489721140687

{"training score": complex_model.score(X_train, y_train),

"testing score": complex_model.score(X_test, y_test)}

{'training score': 0.9954600929824392, 'testing score': 0.9744489721140687}

complex_model.fit(fixed_Xs, Ys)

LGBMRegressor(random_state=2147483648)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

LGBMRegressor(random_state=2147483648)

save_model(complex_model, "lgb.pkl")

model saved....

Observations:

- Baseline boosting model is accurate enough to generalize on unseen data.

Predict on unseen Out-of-Sample Data:

golden_data = pd.read_csv("../../Data/scoring_dataset.csv")

golden_data = prepare_out_of_sample_data(golden_data)

predictions = complex_model.predict(golden_data)

predictions

array([ 58.91912859, 49.89491262, 55.44678162, -24.23093475,

-14.2723258 , -8.53386753, -13.64680361, -9.4624002 ,

17.76568715, 11.00738228, -19.44384469, 13.65440611,

10.68901548, 42.35671464, 64.73750346, 31.21405441,

33.57720901, 66.54627244, 17.34307286, -17.41840316,

10.57054402, 27.4537283 , 69.35269097, -12.27879405,

15.81947529, -9.96537782, -3.50549684, 10.60525138,

29.81544625, -11.33242524, 7.88417464, 11.87869155,

-21.32857179, 68.10191868, 34.02686042, 12.06295287,

9.21788335, 11.4395712 , -22.66475147, 10.90707741,

-11.89317256, -21.2898417 , -16.45650735, 58.73523363,

11.32063774, 51.41548191, -6.16929583, -17.21084875,

8.84313568, -0.23152295, 16.33390489, -7.37397323,

47.33042878, 11.59818288, 35.74334818, 31.79114097,

31.00438204, 30.59942712, 3.56928081, 32.61225069,

30.14717748, -16.59407291, 36.6298427 , 34.46728649,

5.73856431, 3.28154025, -15.33032491, 23.72479771,

-13.24799205, 1.69154499, 28.76880574, 45.32716805,

10.66541024, -16.7040101 , 13.71867892, 38.66482697,

64.90888121, 18.33568536, 64.48881502, -12.42543113,

13.08235257, 32.67607121, 7.26262942, 0.93023009,

-17.55597795, 52.73909182, 54.72162463, 56.50324747,

-16.27963481, -3.71731225, 1.58822318, 46.84579724,

5.79652318, 4.07176173, 11.33118164, -9.52012316,

72.39011481, -13.65875517, 70.09885245, 15.08417505,

5.53303608, 22.4515763 , -10.57416188, -7.47169768,

-3.75537854, 11.61249461, 11.04423492, -14.5301915 ,

67.9224915 , 68.21783413, 64.9184886 , 45.26689911,

14.07367844, -21.0615744 , -9.68622993, 7.99011859,

70.128609 , 1.33740385, -12.34573747, -16.53098494,

0.64245634, -11.7774245 , -17.50944337, 10.03978082,

12.20080724, 0.85478322, -14.41113003, 17.45473449,

11.11047532, -13.92590323, -26.3335464 , -0.49609702,

67.70577189, 8.76217364, 11.37061747, 13.94466969,

31.95999566, -4.73164322, -4.78788719, 35.05434567,

-17.65590835, 11.19294598, -23.46091508, -14.90541622,

59.80512017, -4.39993801, 65.87373554, -10.21459077,

3.34296328, 3.46447491, 18.02436197, 70.92517188,

-16.13044562, 15.22610701, 67.3571339 , 31.31605017,

16.25664797, 65.32404436, -2.44943542, 11.07774281,

-1.36484196, 46.27491016, 11.75272127, 31.86936077,

37.50262643, -12.96696298, 57.84506126, 69.08963572,

-11.01156093, -4.98246628, -2.70502784, -19.59879822,

67.11843829, 12.43076254, -2.18990868, -5.76053432,

30.75636258, 2.32066105, -27.34262945, 23.86179321,

6.83557926, 38.6771704 , 5.4039176 , -19.74764152,

-1.87067716, 36.43479928, -6.51198102, 1.46725762,

54.16904585, 10.90929559, 63.31117438, 11.46281534,

30.56631811, 19.12706775, 44.89570016, -2.61577375,

2.26721515, 30.26308875, 58.11514791, 5.97828353,

-11.03024255, -2.95225412, 49.22757724, 12.35191354,

60.96914324, 7.13226438, -12.56451221, 66.19490992,

-17.87080904, 27.71120954, 1.35281436, 35.80188293,

-16.9561018 , -15.39986594, 0.58514808, 32.63009318,

12.20705734, -4.23991439, 66.45667292, 67.1467423 ,

32.08794442, 71.41162079, -6.69518428, -6.21886221,

0.12338652, -17.3127624 , 5.34228616, -5.28529409,

12.78867194, -0.79418746, 9.26418582, -5.09157918,

46.85243872, 8.764054 , 3.67975868, -14.2596615 ,

10.76950969, 40.52879738, 66.68991439, 23.82932953,

3.60368565, 42.69170346, 8.47585468, 64.57462177,

-7.65456788, -6.94218944, 53.62941074, -9.46495613,

33.06521281, 53.70369254, 21.28483189, 35.32587129,

8.0646854 , 69.71120081, 48.09456914, 66.440138 ,

-11.75407332, 29.66519856, 20.11456971, -15.5240168 ,

-5.4359874 , -14.34577371, -0.26161014, -4.41381492,

-16.60818486, -17.69304935, -7.09102285, -6.55568194,

-11.53152147, 59.64454771, 15.40693518, 68.11999211,

36.45709991, -6.1543164 , -16.20525925, -11.24193557,

18.08161099, 40.05749666, 35.53561637, 47.87203529,

-4.38230475, 7.44872708, 7.24849564, 7.74243436,

43.23607339, -7.2239746 , -12.54961912, 11.10762799,

51.24267263, -3.18134816, -5.56914843, 66.37558673,

34.01434221])

golden_data_output = golden_data.copy()

golden_data_output["Predictions"] = predictions

golden_data_output.to_csv("../../Output Files/Data/prediction.csv")

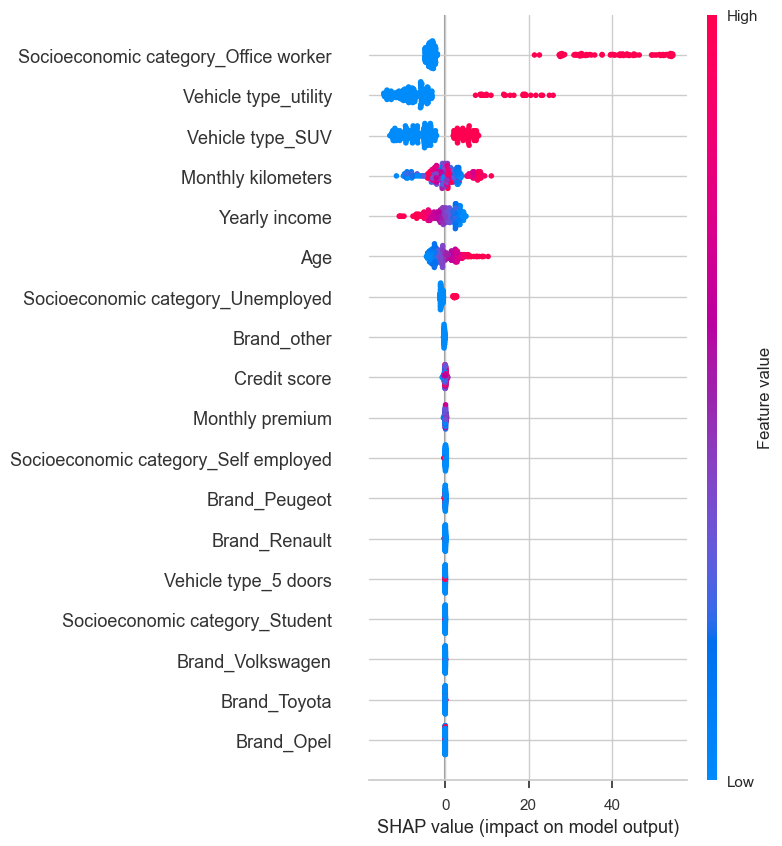

Analyze Predictions with SHAP values:

shap.initjs()

explainer = shap.TreeExplainer(complex_model)

shap_values = explainer.shap_values(golden_data, predictions, check_additivity=False)

shap.summary_plot(shap_values, golden_data, max_display=len(golden_data.index))

Observations:

- Vehicle type 5 doors and SUV to blame for low Net-profit forecasting.

- Numerical variables Age and monthly kilometers and CRM score contributed the most for higher net profit.

- Other features such as Brands, Socioeconomic status has no effect compared to variables on the top.

- From feature importance plot it shows Yearly income, monthly kilometers, Age and CRM score are the most important factors in deciding net profit.

- It would be insightful to understand what to blame for high or low net profit from an out-of-sample dataset, as per individual forecasts.

- Higher age and monthly kilometers contributes higher net-profit, tho there are some cases where high value of age “red” decreases nonprofit, a dependence plot between two features will show how two similar values of monthly kilometers contributes differently to profit as it depends on interaction of two features.

Individual Explanations of High and Low net profit forecasts.

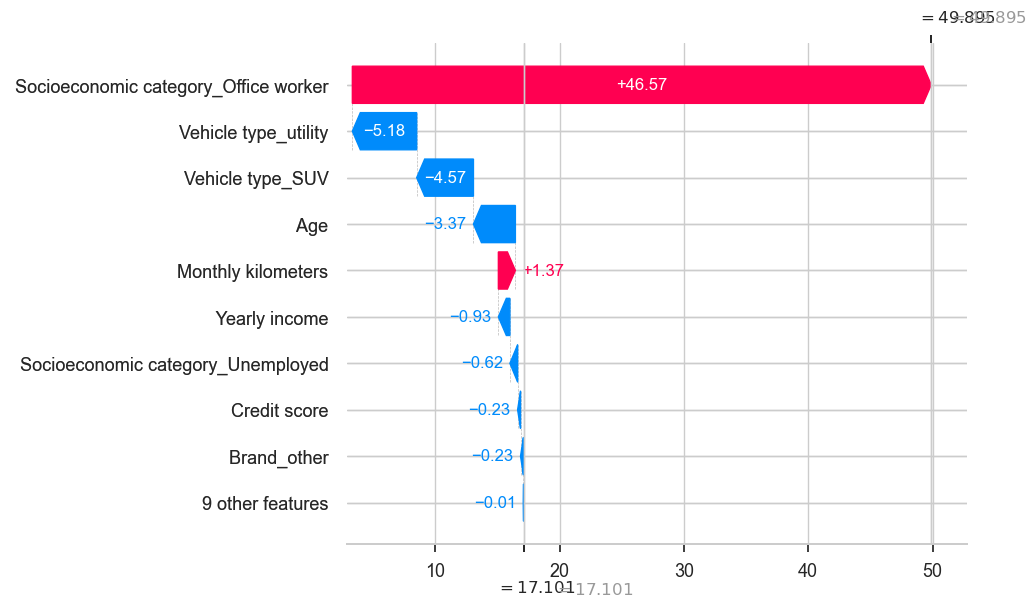

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[1],

golden_data.iloc[1],

golden_data.columns)

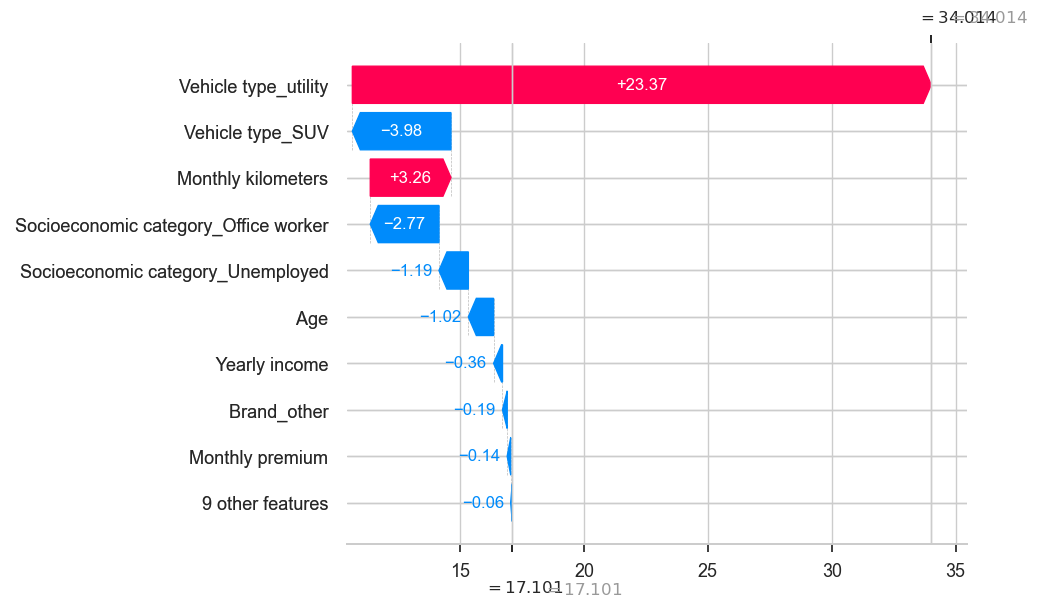

print(predictions[1])

golden_data.iloc[1]

Predicted-Profit 49.894912616226186

Age 21.0

Monthly premium 14.0

Monthly kilometers 694.0

Yearly income 34900.0

Credit score 833.0

Brand_Opel 1.0

Brand_Peugeot 0.0

Brand_Renault 0.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 1.0

Vehicle type_SUV 0.0

Vehicle type_utility 0.0

Socioeconomic category_Office worker 1.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 0.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1001, dtype: float64

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[292],

golden_data.iloc[292],

golden_data.columns)

print(predictions[292])

golden_data.iloc[292]

Predicted-Profit 34.0143422063608

Age 33.0

Monthly premium 8.0

Monthly kilometers 748.0

Yearly income 32360.0

Credit score 271.0

Brand_Opel 1.0

Brand_Peugeot 0.0

Brand_Renault 0.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 0.0

Vehicle type_SUV 0.0

Vehicle type_utility 1.0

Socioeconomic category_Office worker 0.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 1.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1298, dtype: float64

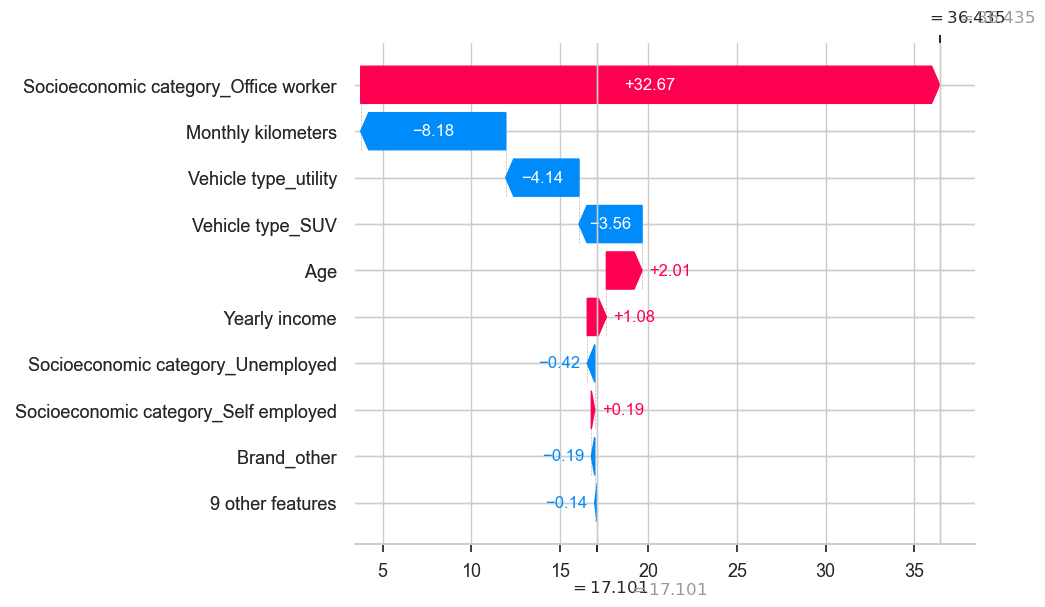

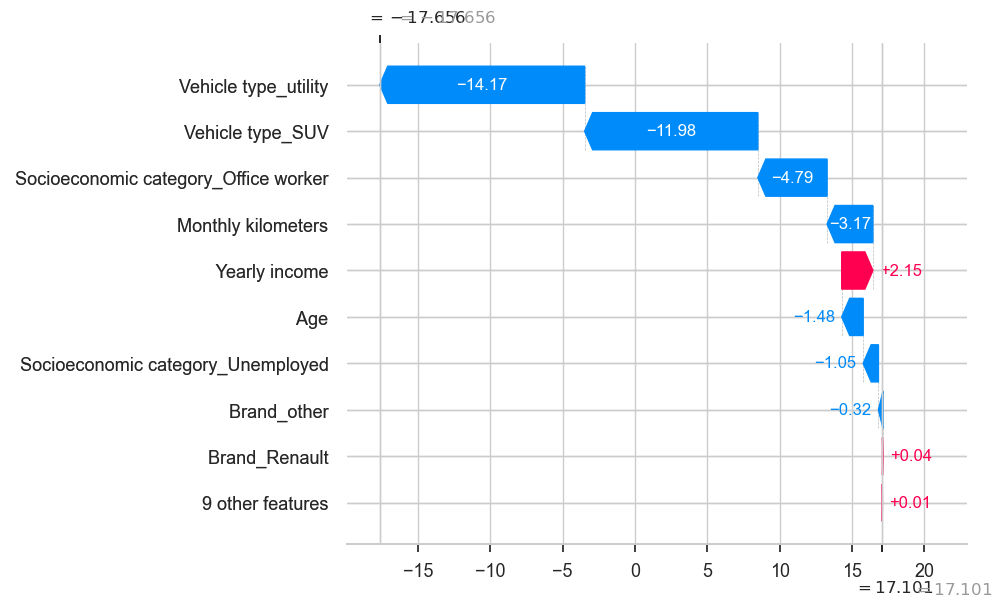

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[185],

golden_data.iloc[185],

golden_data.columns)

print(predictions[185])

golden_data.iloc[185]

Predicted-Profit 36.434799275715484

Age 42.0

Monthly premium 15.0

Monthly kilometers 345.0

Yearly income 21730.0

Credit score 78.0

Brand_Opel 0.0

Brand_Peugeot 0.0

Brand_Renault 0.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 0.0

Vehicle type_SUV 0.0

Vehicle type_utility 0.0

Socioeconomic category_Office worker 1.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 0.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1190, dtype: float64

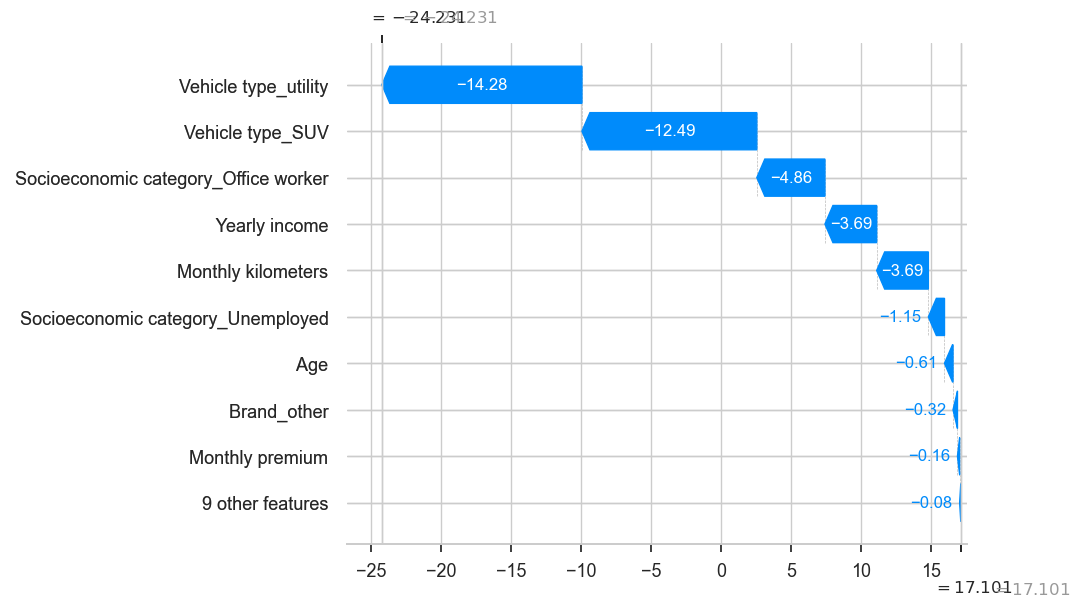

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[3],

golden_data.iloc[3],

golden_data.columns)

print(predictions[3])

golden_data.iloc[3]

Predicted-Profit -24.23093475368557

Age 33.0

Monthly premium 2.0

Monthly kilometers 970.0

Yearly income 45450.0

Credit score 990.0

Brand_Opel 0.0

Brand_Peugeot 0.0

Brand_Renault 0.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 1.0

Vehicle type_SUV 0.0

Vehicle type_utility 0.0

Socioeconomic category_Office worker 0.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 1.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1003, dtype: float64

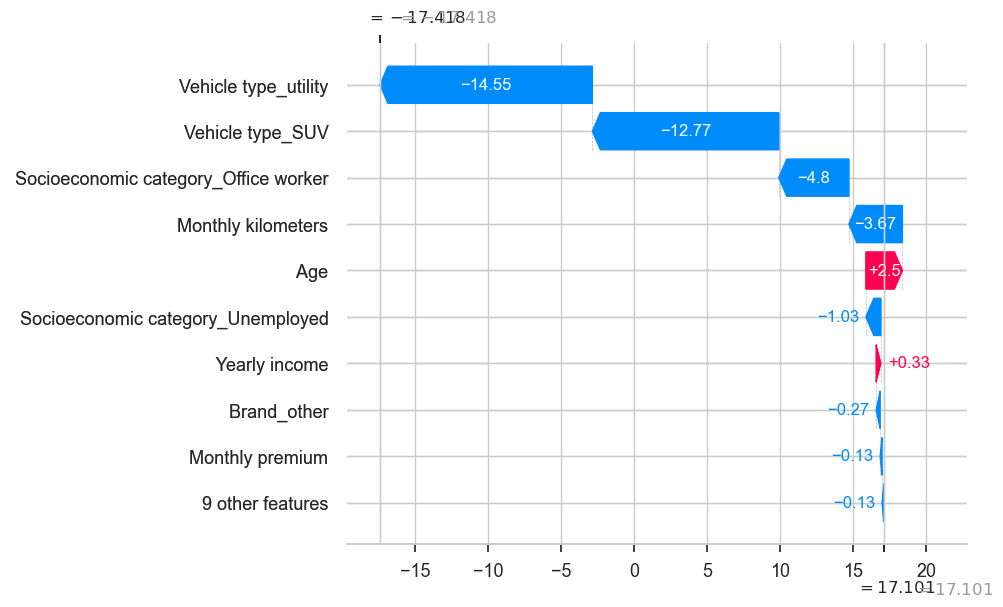

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[19],

golden_data.iloc[19],

golden_data.columns)

print(predictions[19])

golden_data.iloc[19]

Predicted-Profit -17.41840315625436

Age 45.0

Monthly premium 4.0

Monthly kilometers 993.0

Yearly income 29160.0

Credit score 255.0

Brand_Opel 0.0

Brand_Peugeot 0.0

Brand_Renault 1.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 0.0

Vehicle type_SUV 0.0

Vehicle type_utility 0.0

Socioeconomic category_Office worker 0.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 0.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1021, dtype: float64

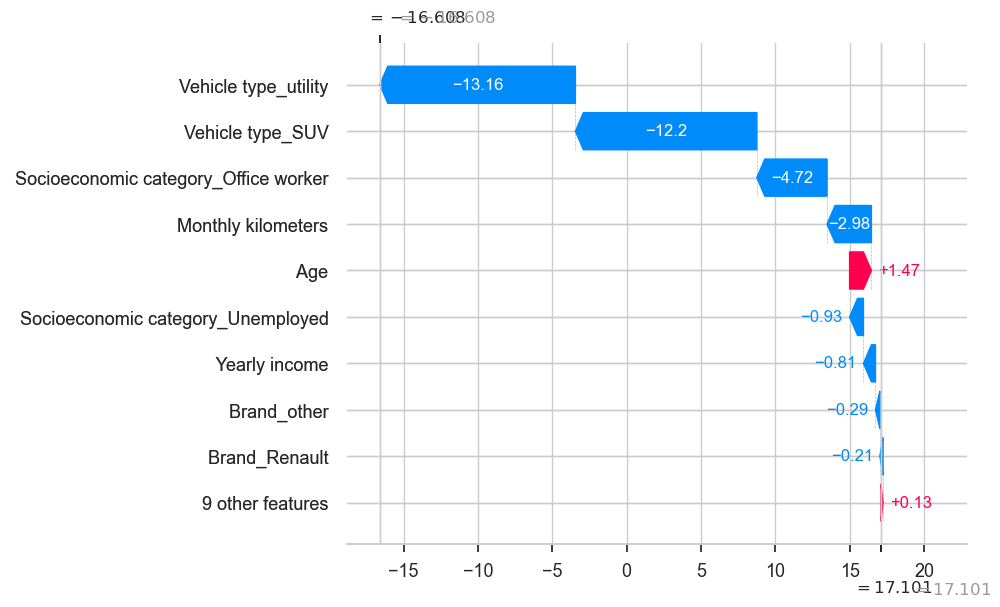

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[140],

golden_data.iloc[140],

golden_data.columns)

print(predictions[140])

golden_data.iloc[140]

Predicted-Profit -17.65590834806663

Age 30.0

Monthly premium 27.0

Monthly kilometers 915.0

Yearly income 19460.0

Credit score 746.0

Brand_Opel 0.0

Brand_Peugeot 1.0

Brand_Renault 0.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 0.0

Vehicle type_SUV 0.0

Vehicle type_utility 0.0

Socioeconomic category_Office worker 0.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 0.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1145, dtype: float64

shap.plots._waterfall.waterfall_legacy(explainer.expected_value,

shap_values[264],

golden_data.iloc[264],

golden_data.columns)

print(predictions[264])

golden_data.iloc[264]

Predicted-Profit -16.60818486301198

Age 41.0

Monthly premium 5.0

Monthly kilometers 801.0

Yearly income 32950.0

Credit score 824.0

Brand_Opel 0.0

Brand_Peugeot 0.0

Brand_Renault 1.0

Brand_Toyota 0.0

Brand_Volkswagen 0.0

Vehicle type_5 doors 0.0

Vehicle type_SUV 0.0

Vehicle type_utility 0.0

Socioeconomic category_Office worker 0.0

Socioeconomic category_Self employed 0.0

Socioeconomic category_Student 0.0

Socioeconomic category_Unemployed 0.0

Brand_other 0.0

Name: 1270, dtype: float64